Need extra housing market tales from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

After taking an enormous macro hit through the 2022 rate-shock, United Wholesale Mortgage’s (UWM) refinance quantity has discovered its footing—and retains climbing:

- 2020: $140B

- 2021: $139B

- 2022: $36B

- 2023: $14B (cycle low)

- 2024: $43B

- 2025: $70B

That’s a +387% enhance in UWM’s refi quantity since its 2023 cycle low.

Even and not using a full refi growth, refinance quantity is slowly coming again, with the average 30-year fixed mortgage rate as tracked by Freddie Mac down to five.98% final week—or 1.81 bps under its cycle excessive of seven.79% in October 2023.

Many latest debtors who took on larger mortgage charges (2023–2024 vintages) are leaping on the alternative to refinance and safe some fee reduction. On the identical time, UWM’s buy quantity has remained comparatively regular within the $90B–$96B vary over the previous few years.

The dearth of a pointy decline in buy quantity following the rate-shock is spectacular when you think about the macro image: Whereas U.S. present dwelling gross sales fell sharply in 2022, UWM’s buy quantity held regular because the wholesale channel gained share through the downturn. Many smaller lenders pulled again or exited, and brokers consolidated quantity towards giant, price-competitive gamers. UWM stored pushing ahead. That buy stability provides UWM an important base to function from as refis enhance.

Whereas UWM’s refinance rebound is going on sooner than most mortgage companies (and in consequence, it’s taking refinance market share), refinance exercise general is slowly bouncing off the rate-shock lows.

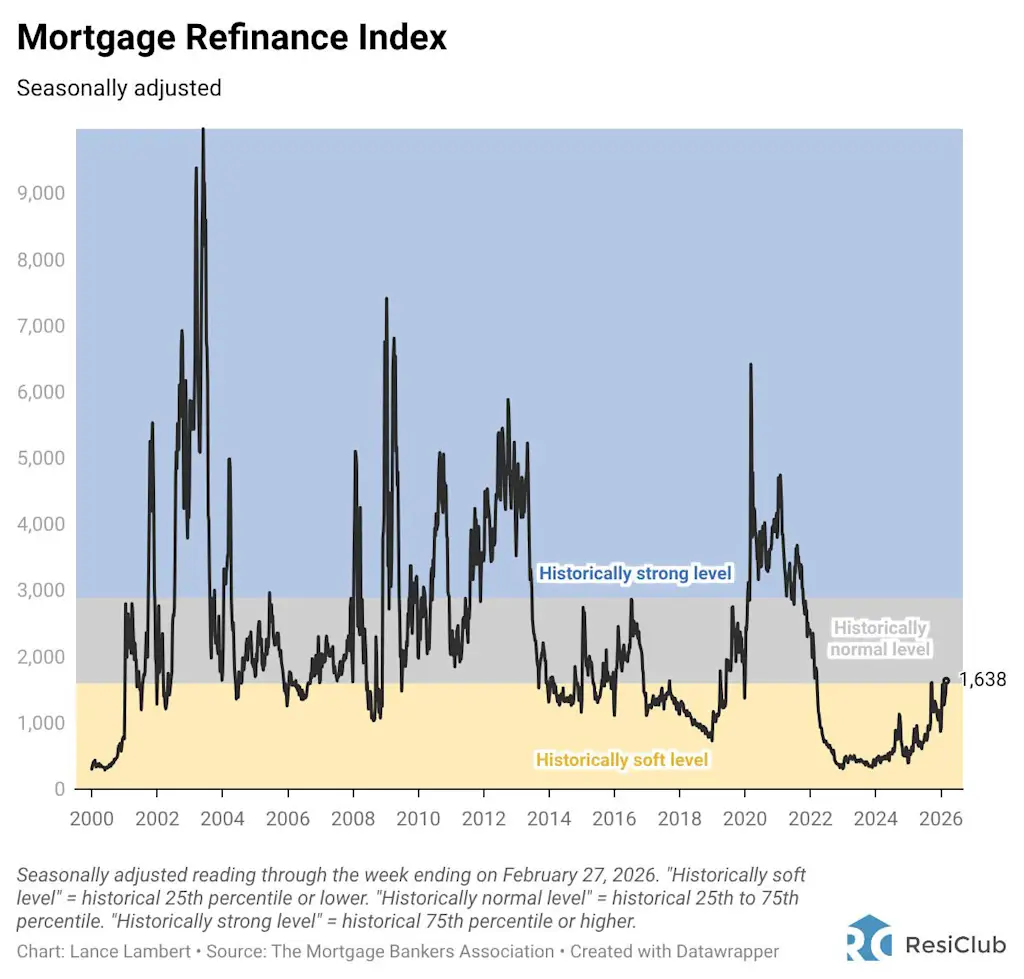

The Mortgage Refinance Index studying for the fourth week of February, by yr:

- February 2018 —> 1,169

- February 2019 —> 1,134

- February 2020 —> 3,594

- February 2021 —> 3,850

- February 2022 —> 1,686

- February 2023 —> 400

- February 2024 —> 396

- February 2025 —> 784

- February 2026 —> 1,638

Zoomed out, mortgage refinance functions began 2026 nonetheless in “traditionally gentle” territory (backside twenty fifth percentile). Nonetheless, over the previous week, they crossed the edge into the underside of “traditionally regular” refinance ranges (twenty fifth–seventy fifth percentile).

ResiClub prefers to name this upswing a “refi boomlet” reasonably than a “refi growth.” We use the time period boomlet as a result of there’s a ceiling on how large this refinance pop can get—and the way lengthy it could final—and not using a extra substantial drop in mortgage charges. In spite of everything, in keeping with the newest FHFA knowledge, 68.6% of U.S. mortgage borrowers still hold an interest rate below 5.0%.

That stated, the extra time U.S. householders have to regulate to immediately’s mortgage charges, the extra some could also be enticed to refinance or faucet their fairness by way of a HELOC or dwelling fairness mortgage.