Need extra housing market tales from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

When assessing dwelling value momentum, ResiClub believes it’s necessary to observe lively listings and months of provide. If lively listings begin to quickly improve as houses stay available on the market for longer durations, it could point out pricing softness or weak point. Conversely, a fast decline in lively listings past seasonality may recommend a market that’s heating up.

For the reason that pandemic housing increase fizzled out in 2022, the nationwide energy dynamic has slowly been shifting directionally from sellers to patrons. After all, throughout the nation, that shift has different.

Typically talking, native housing markets the place lively stock has jumped above pre-pandemic 2019 ranges have experienced softer home price growth (or outright value declines) over the previous 36 months. Conversely, native housing markets the place lively stock stays far beneath pre-pandemic 2019 ranges have, usually talking, skilled, comparatively talking, extra resilient dwelling value progress over the previous 42 months.

The place is nationwide lively stock headed?

Nationwide lively listings are on the rise on a year-over-year foundation (+7.9% between February 28, 2025, and February 28, 2026). This means that homebuyers have gained some leverage in lots of elements of the nation over the previous 12 months. Some vendor’s markets have became balanced markets, and extra balanced markets have became purchaser’s markets.

Nationally, we’re nonetheless beneath pre-pandemic 2019 stock ranges (-17.0% beneath February 2019), and a few resale markets—particularly, chunks of the Midwest and Northeast—nonetheless stay, comparatively talking, tight-ish.

Whereas nationwide lively stock continues to be up 12 months over 12 months, the tempo of progress has slowed in current months as softening has slowed.

Listed here are the full variety of February stock/lively listings over the previous decade, in keeping with Realtor.com:

- February 2017 -> 1,151,120 📉

- February 2018 -> 1,045,153 📉

- February 2019 -> 1,102,660 📈

- February 2020 -> 928,343 📉

- February 2021 -> 464,919 📉 (Pandemic housing increase overheating)

- February 2022 -> 346,511 📉 (Pandemic housing increase overheating)

- February 2023 -> 579,264 📈

- February 2024 -> 664,716 📈

- February 2025 -> 847,825 📈

- February 2026 -> 914,860 📈

If we preserve the present year-over-year tempo of stock progress (+67,035 houses on the market), we’d have 981,895 lively stock listings come February 2027. (That’s not a prediction—I’m simply displaying what the mathematics appears to be like like if that tempo continued.)

Beneath is the year-over-year lively stock share change by state.

window.addEventListener(“message”,operate(a){if(void 0!==a.knowledge[“datawrapper-height”]){var e=doc.querySelectorAll(“iframe”);for(var t in a.knowledge[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.supply){var d=a.knowledge[“datawrapper-height”][t]+”px”;r.fashion.top=d}}});

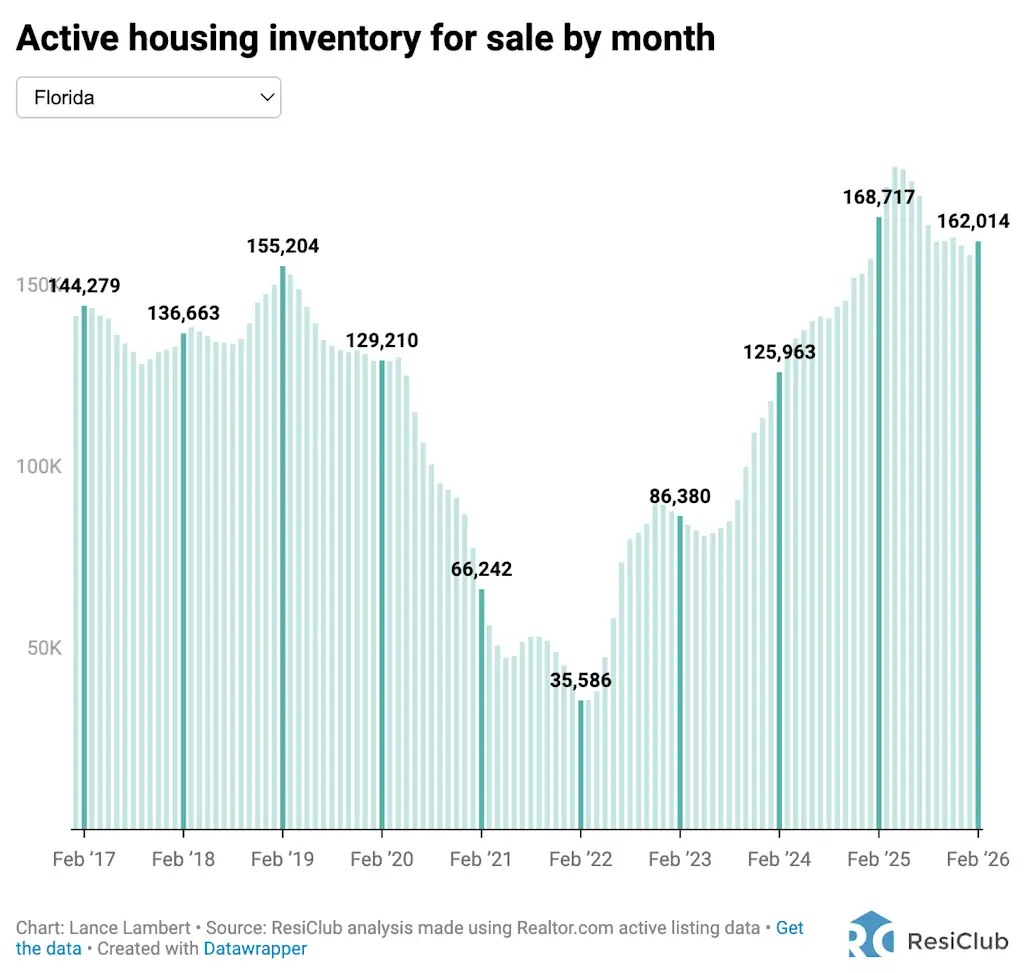

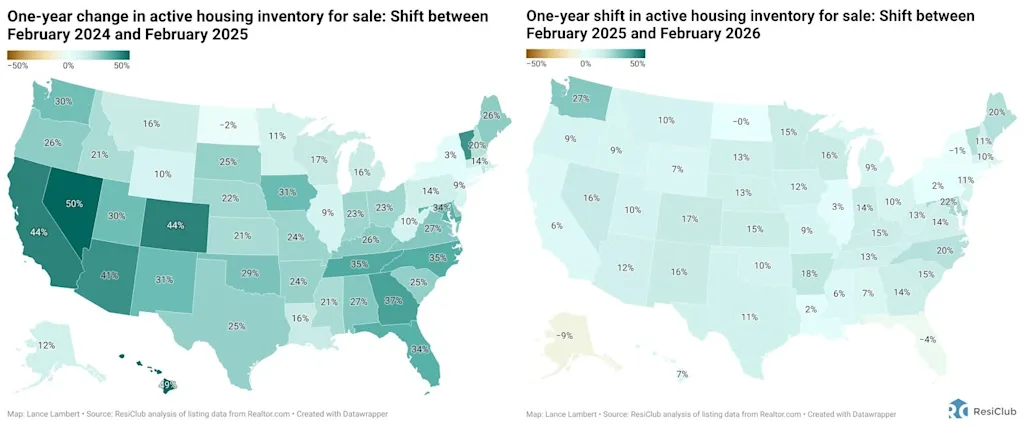

Whereas lively housing stock is rising in most markets on a year-over-year foundation, the tempo of progress continues to decelerate throughout a lot of the nation (see the side-by-side maps beneath). In actual fact, Florida—dwelling to lots of the weakest regional housing markets over the previous two years—is now seeing lively stock edge down somewhat, 12 months over 12 months (-4%).

LEFT: Year-over-year active inventory shift between February 2024 and February 2025

RIGHT: Year-over-year active inventory shift between February 2025 and February 2026

And whereas lively housing stock is rising in most markets on a year-over-year foundation, some markets nonetheless stay tight-ish (though it’s loosening in these locations, too).

As ResiClub has been documenting, each lively resale and new houses on the market stay probably the most restricted throughout big swaths of the Midwest and Northeast. That’s the place dwelling sellers within the spring are possible, comparatively talking, to have extra energy than their friends in lots of Southern markets.

In distinction, lively housing stock on the market has neared or surpassed pre-pandemic 2019 ranges in lots of elements of the Solar Belt and Mountain West, together with metro-area housing markets akin to Austin and Punta Gorda, Florida.

Many of those areas noticed main value surges throughout the pandemic housing increase, with dwelling costs getting stretched in comparison with native incomes. As pandemic-driven home migration slowed and mortgage charges rose, markets like Punta Gorda and Austin confronted challenges, counting on native revenue ranges to help frothy dwelling costs.

This softening pattern was accelerated additional by an abundance of recent dwelling provide within the Solar Belt. Builders are sometimes keen to decrease costs or supply affordability incentives (if they’ve the margins to take action) to take care of gross sales in a shifted market, which additionally has a cooling impact on the resale market. Some patrons, who would have beforehand thought of present houses, are actually choosing new houses with extra favorable offers—which then places some extra upward stress on resale stock.

window.addEventListener(“message”,operate(a){if(void 0!==a.knowledge[“datawrapper-height”]){var e=doc.querySelectorAll(“iframe”);for(var t in a.knowledge[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.supply){var d=a.knowledge[“datawrapper-height”][t]+”px”;r.fashion.top=d}}});

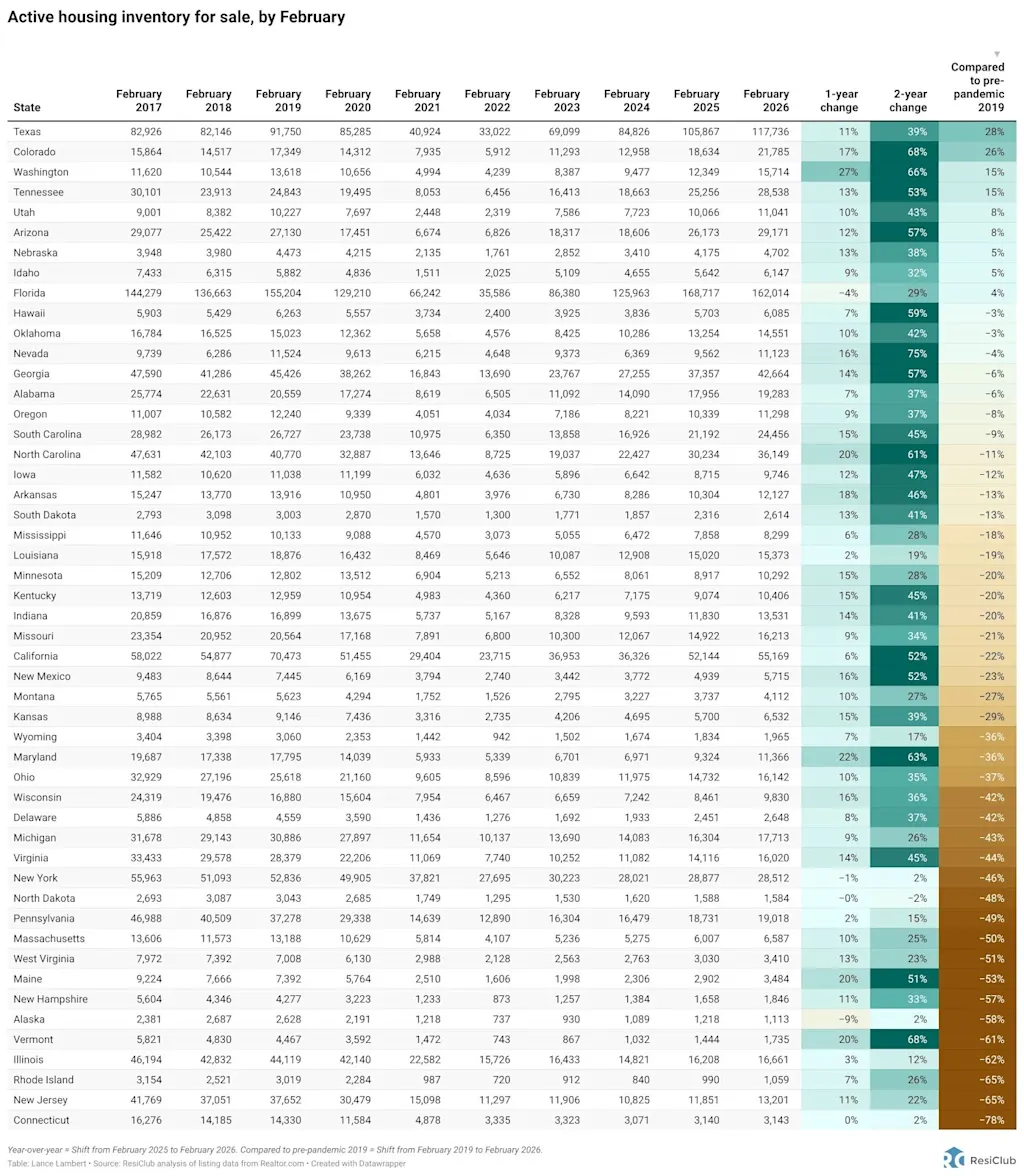

On the finish of February 2026, 9 states had been above pre-pandemic 2019 lively stock ranges: Arizona, Colorado, Florida, Idaho, Nebraska, Tennessee, Texas, Utah, and Washington. (The District of Columbia—which we omitted of this desk beneath—is again above pre-pandemic 2019 lively stock ranges, too. Softness in D.C. proper predates the present admin’s job cuts.)

window.addEventListener(“message”,operate(a){if(void 0!==a.knowledge[“datawrapper-height”]){var e=doc.querySelectorAll(“iframe”);for(var t in a.knowledge[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.supply){var d=a.knowledge[“datawrapper-height”][t]+”px”;r.fashion.top=d}}});

Huge image: Over the previous few years, we’ve noticed a softening throughout many housing markets, as strained affordability has tempered the fervor of a market that was unsustainably scorching throughout the pandemic housing increase and incomes have had an opportunity to slowly catch up. Whereas home prices are falling some in pockets of the Sun Belt, a giant chunk of Northeast and Midwest markets are nonetheless eking out somewhat year-over-year appreciation. Nationally aggregated dwelling costs are fairly near flat, 12 months over 12 months.

Beneath is one other model of the desk above—however this one consists of each month since January 2017.

window.addEventListener(“message”,operate(a){if(void 0!==a.knowledge[“datawrapper-height”]){var e=doc.querySelectorAll(“iframe”);for(var t in a.knowledge[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.supply){var d=a.knowledge[“datawrapper-height”][t]+”px”;r.fashion.top=d}}});

In the event you’d wish to additional look at the month-to-month state stock figures, use the interactive beneath.

Over the approaching months, let’s control Florida, which has now entered its seasonal window when its lively stock sometimes begins to rise once more. (To this point, the seasonal bounce has been tame.) To higher perceive softness and weak point throughout Florida over the previous couple of years, read this ResiClub PRO report.

Click here to view an interactive/searchable model of the chart beneath