Need extra housing market tales from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

Because the Pandemic Housing Increase fizzled out in the summertime of 2022, some overheated elements of the nation—notably within the West, Southwest, and Southeast—have skilled house worth declines from their peak (see this map). Whereas many of those markets have seen solely modest drops, a couple of metro areas, comparable to Cape Coral and Austin, have undergone what I’d think about “materials” house worth corrections, falling -19.1% and -27.8%, respectively, from their peaks.

These regional house worth declines elevate the query: What number of mortgage debtors are literally “underwater” proper now?

To seek out out, ResiClub once again reached out to ICE Mortgage Technology—previously generally known as Black Knight, earlier than it was acquired by Intercontinental Change for $11.8 billion in 2023.

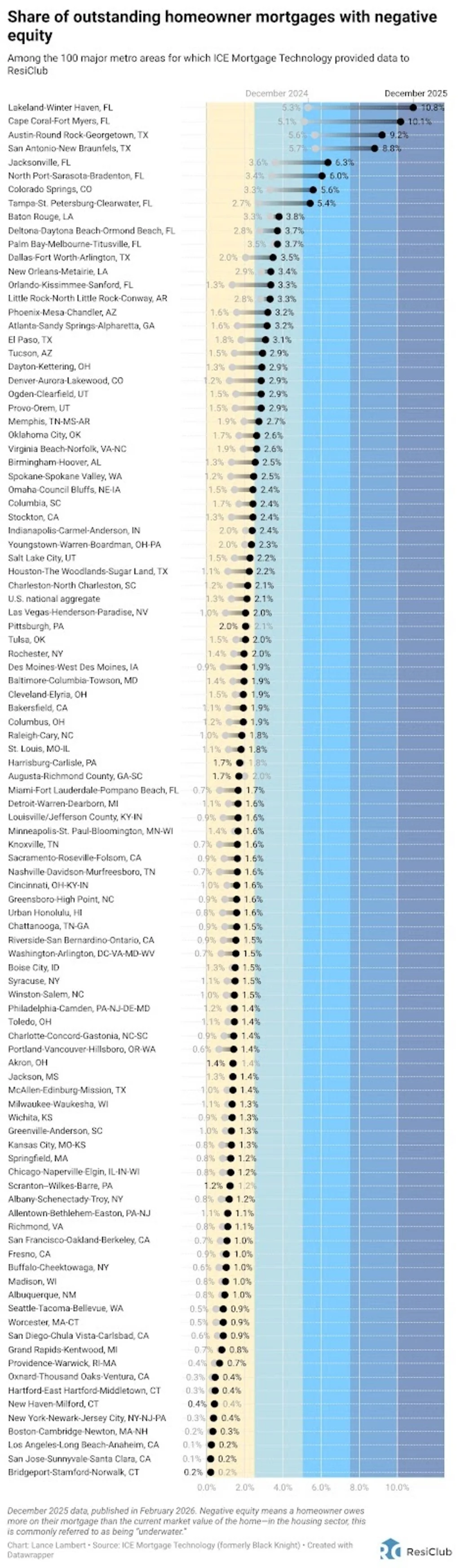

2.1% —> The share of excellent U.S. house owner mortgages with unfavourable fairness* (i.e. underwater) on the finish of December 2025, in accordance with knowledge from ICE Mortgage Expertise supplied to ResiClub this week. Again in December 2024, that determine was 1.3%.

23.0% —> The share of excellent house owner mortgages with unfavourable fairness (i.e. underwater) on the finish of September 2009, according to Cotality/FirstAmerica.

Why, on a nationally aggregated foundation, are there nonetheless not many householders underwater regardless of house worth declines in some markets?

- Nationally combination current house costs are nonetheless fairly near all-time highs. Whereas many pockets of the West, Southwest, and Southeast have seen house costs decline at the least some from their Pandemic Housing Increase peak, nationally aggregated single-family costs are nonetheless fairly near all-time highs.

- Amortization of extremely low mortgage charges. Many owners locked in ultra-low mortgage charges throughout the Pandemic Housing Increase. With mounted charges round 2% to three%, these month-to-month funds included a bigger proportion of principal compensation from the beginning. Meaning debtors have been paying down their balances extra aggressively than they might underneath higher-rate loans. As of This fall 2025, 51.5% of excellent mortgage holders nonetheless have charges under 4.0%, which has helped some debtors construct fairness quicker and provides them a better buffer.

- Few patrons truly bought on the peak in correction markets. Even in boom-to-correction markets like Austin, TX or Cape Coral, FL, solely a small share of householders purchased on the absolute prime of the market in spring 2022. Most present householders in these areas both purchased earlier than the height. This restricted publicity on the peak helps clarify why unfavourable fairness, to this point, hasn’t been an enormous downside, even in a number of the hardest-hit metros.

Whereas solely 2.1% of excellent U.S. house owner mortgages have unfavourable fairness, there are a couple of pockets the place that share is approaching 10.0%—or has even barely exceed it.

Among the many 100 main metro areas for which ICE Mortgage Expertise supplied knowledge to ResiClub, these 10 metros have the very best share of house owner mortgages at present underwater:

- Lakeland-Winter Haven, FL —> 10.8%

- Cape Coral-Fort Myers, FL —> 10.1%

- Austin-Spherical Rock-Georgetown, TX —> 9.2%

- San Antonio-New Braunfels, TX —> 8.8%

- Jacksonville, FL —> 6.3%

- North Port-Sarasota-Bradenton, FL —> 6.0%

- Colorado Springs, CO —> 5.6%

- Tampa-St. Petersburg-Clearwater, FL —> 5.4%

- Baton Rouge, LA —> 3.8%

- Deltona-Daytona Seashore-Ormond Seashore, FL —> 3.7%

- Palm Bay-Melbourne-Titusville, FL —> 3.7%

- Dallas-Fort Value-Arlington, TX —> 3.5%

- New Orleans-Metairie, LA —> 3.4%

- Orlando-Kissimmee-Sanford, FL —> 3.3%

- Little Rock-North Little Rock-Conway, AR —> 3.3%

Even in markets like Cape Coral (10.1%) and Austin (9.2%) which have increased shares of excellent house owner mortgages which might be at present underwater, that’s nonetheless far off from the degrees seen on the top of the GFC period bust. For comparability, again in September 2009 a staggering 68% of mortgage debtors in Nevada, 48% in Arizona, and 45% in Florida had been underwater.

To date, within the down markets, it’s actually simply the 2022, 2023, and 2024 vintages being impacted (for proof, look at this chart we made last summer).

Massive image: If house costs in elements of the Southwest, Southeast, and West proceed to expertise gentle house worth pullbacks, the share of current debtors who’re underwater in these markets will rise past the degrees we’ve outlined at present. Nevertheless, barring a significant downward shift, it nonetheless wouldn’t anytime quickly come near the depths of unfavourable fairness seen in 2009 or 2010.