Need extra housing market tales from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

In the course of the Pandemic Housing Increase, from summer time 2020 to spring 2022, the variety of lively houses on the market in most housing markets plummeted as homebuyer demand rapidly absorbed nearly every little thing that got here up on the market and sellers had final energy.

Quick-forward to the present housing market, and the locations the place lively stock has rebounded to 2019 ranges (as a result of strained affordability suppressing purchaser demand) are actually the very locations the place homebuyers have gained essentially the most energy.

On the finish of November 2025, nationwide lively housing stock on the market was nonetheless -6% below November 2019 levels. Nevertheless, increasingly regional markets are surpassing that threshold.

This checklist is rising:

January 2025: 41 of the 200 largest metro space housing markets have been again above pre-pandemic 2019 stock ranges.

February 2025: 44 of the 200 largest metro space housing markets have been again above pre-pandemic 2019 stock ranges.

March 2025: 58 of the 200 largest metro space housing markets have been again above pre-pandemic 2019 stock ranges.

April 2025: 69 of the 200 largest metro space housing markets have been again above pre-pandemic 2019 stock ranges.

Might 2025: 75 of those 200 main markets have been again above pre-pandemic 2019 stock ranges.

June 2025: 78 of those 200 main markets have been again above pre-pandemic 2019 stock ranges.

July 2025: 80 of those 200 main markets have been again above pre-pandemic 2019 stock ranges.

August 2025: 80 of those 200 main markets have been again above pre-pandemic 2019 stock ranges.

September 2025: 81 of those 200 main markets have been again above pre-pandemic 2019 stock ranges.

October 2025: 84 of those 200 main markets have been again above pre-pandemic 2019 stock ranges.

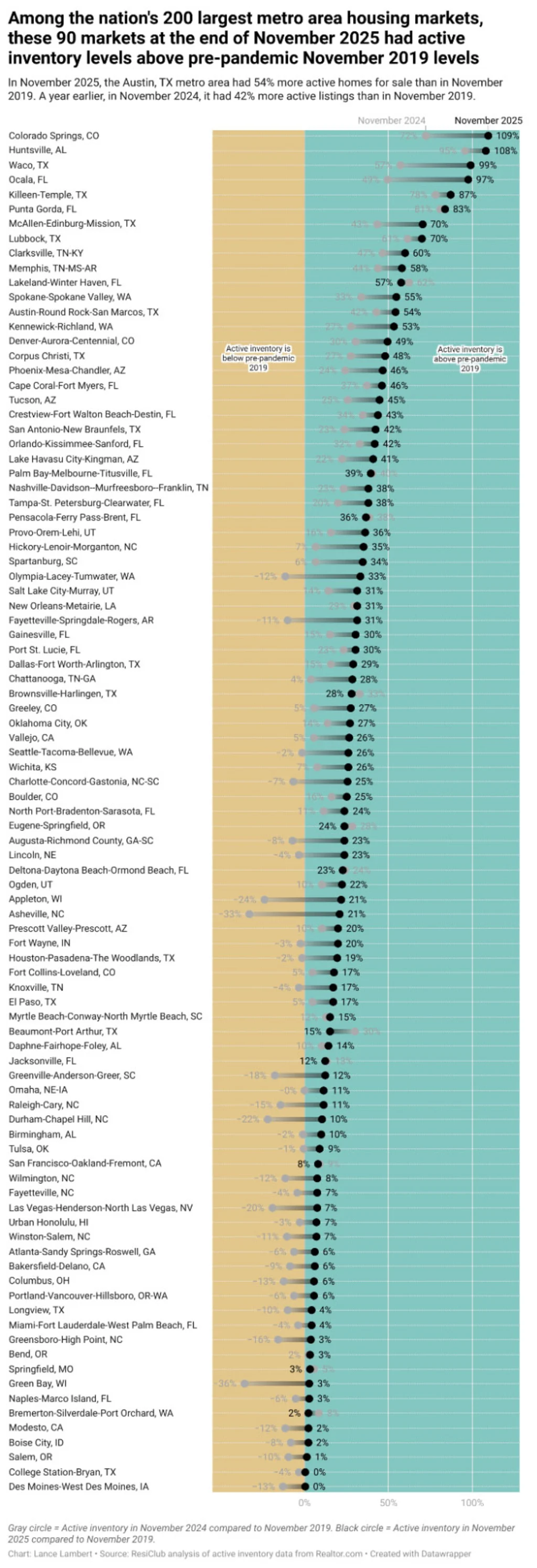

Now, on the newest studying for the tip of November 2025, 90 of the 200 markets are above pre-pandemic 2019 stock ranges.

Whereas this checklist of housing markets again above pre-pandemic 2019 stock ranges was rising by a lot of the 12 months, it has stalled a bit not too long ago. The explanation? Stock development has slowed in current months—greater than typical seasonality would recommend—as some dwelling sellers in tender and weak markets within the Solar Belt have thrown within the towel and delisted (extra on that in one other piece).

This subsequent desk helps you see what the stock image in these similar 90 markets appears like now and what it seemed like final 12 months.

Amongst these 90 markets, you’ll discover tons in Solar Belt markets like Florida, Texas, Arizona, and Colorado.

Lots of the softest housing markets, the place homebuyers have gained leverage, are situated in Gulf Coast and Mountain West areas. A few of these areas have been among the many nation’s high pandemic boomtowns, having skilled important dwelling value development through the pandemic housing growth, which stretched housing fundamentals far past native earnings ranges.

When pandemic-fueled home migration slowed and mortgage charges spiked, markets like Cape Coral, Florida, and San Antonio, Texas, confronted challenges as they needed to depend on native incomes to maintain frothy dwelling costs. The housing market softening in these areas was additional accelerated by the abundance of latest dwelling provide within the pipeline throughout the Solar Belt.

Builders in these areas are sometimes prepared to cut back internet efficient costs or make different affordability changes to take care of gross sales. These changes within the new development market additionally create a cooling impact on the resale market, as some consumers who may need opted for an present dwelling shift their focus to new houses the place offers are nonetheless obtainable.

In distinction, many Northeast and Midwest markets have been much less reliant on pandemic migration and have much less new dwelling development in progress. With decrease publicity to that demand shock, lively stock in these Midwest and Northeast areas has remained comparatively tight, maintaining the benefit within the arms of dwelling sellers.

window.addEventListener(“message”,operate(a){if(void 0!==a.information[“datawrapper-height”]){var e=doc.querySelectorAll(“iframe”);for(var t in a.information[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.supply){var d=a.information[“datawrapper-height”][t]+”px”;r.type.peak=d}}});

Typically talking, housing markets the place stock (i.e., lively listings) has returned to pre-pandemic ranges have skilled softer/weaker dwelling value development (or outright declines) over the previous 36 months. Conversely, housing markets the place stock stays far under pre-pandemic ranges have, usually talking, skilled extra resilient dwelling value development over the previous 36 months.

ResiClub PRO members can discover our newest stock evaluation for +800 metros and +3,000 counties here, and our newest evaluation displaying why the 2019 stock comparability stays insightful here.