Need extra housing market tales from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

We’re presently amid a 14-month streak by which year-over-year nationally aggregated employee earnings development (+3.4% YoY) has exceeded year-over-year nationally aggregated residence worth development (+1.3% YoY).

This era of housing market softness—with some pandemic boomtowns within the Solar Belt and Mountain West experiencing outright corrections—helps enhance underlying nationwide housing affordability on paper, which turned stretched following the overheating through the Pandemic Housing Growth and the next mortgage price shock.

To higher perceive how far nationally aggregated housing affordability stays from its long-run historic common, ICE Mortgage Technology calculated how a lot simply one of many three core housing affordability levers would want to shift, on paper, to instantly return affordability to that long-run common:

- U.S. incomes spiked +19%

- U.S. residence costs fell -16%

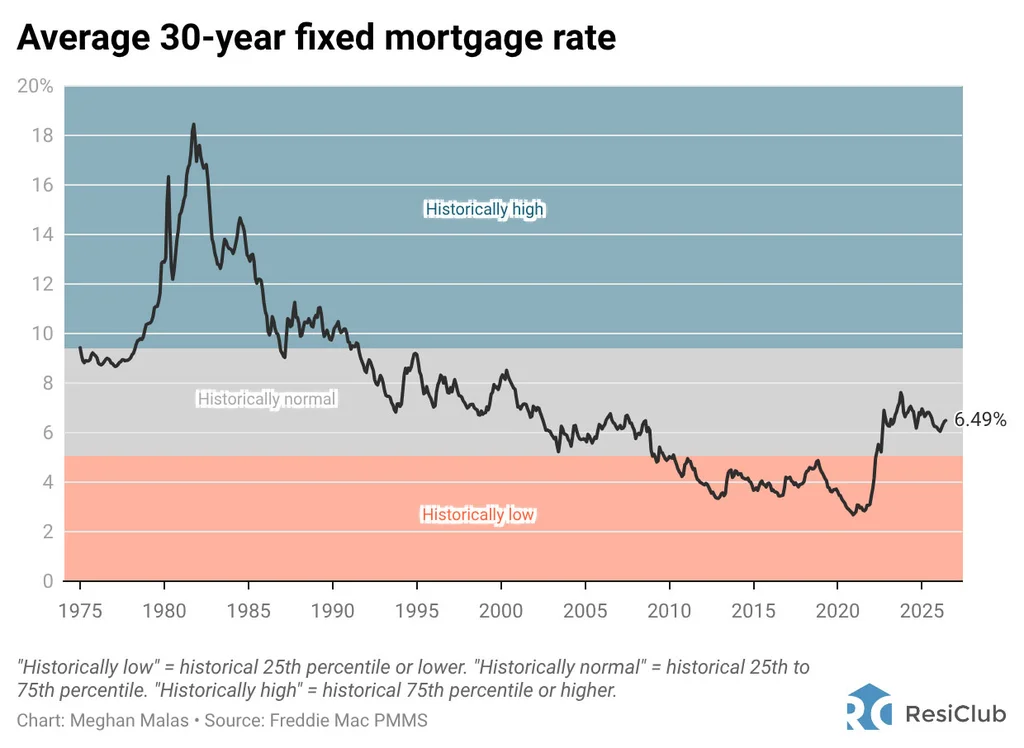

- Mortgage charges fell 1.60 proportion factors (from 6.59% to 4.99%)

To make clear: The calculations above present how a lot only one metric would want to shift—holding all the things else fixed—to return nationally aggregated housing affordability to its long-run historic common.

This can be a back-of-the-envelope train designed as an instance how far affordability presently sits from that long-run common. The purpose isn’t to determine the almost definitely path again to that historic norm, however somewhat to quantify the space between the place affordability is as we speak and the place it has traditionally been.

In keeping with ICE Mortgage’s June 2026 Mortgage Monitor report, buying the average-priced U.S. residence required 29.8% of the median U.S. family revenue wanted to cowl month-to-month principal and curiosity funds on a 20% down, 30-year fixed-rate mortgage.

The silver lining: That’s an enchancment from the cycle excessive of 35.0% in October 2023.

Within the quick time period, the affordability lever that may traditionally have the quickest instant affect is mortgage charges. Nevertheless, until one thing materials shifts within the broader economic system (e.g., a spike in unemployment), most financial fashions stay skeptical of a cloth near-term decline in long-term Treasury yields and mortgage charges.